Business

The importance of insurance when heading abroad

With a rise from 55% to 57% of people jetting off abroad for their holidays, according to figures from the ABTA Holiday Habits report of 2017, holidays are less of a luxury item and more of a simple necessity. But with so many people opting to go abroad, how many of us are taking out travel insurance? What does the insurance cover, and is it worth it? We’ve teamed up with accident at work claims specialists, True Solicitors, to take a look at everything you need to know before risking going abroad without insurance.

Who is or isn’t taking out insurance?

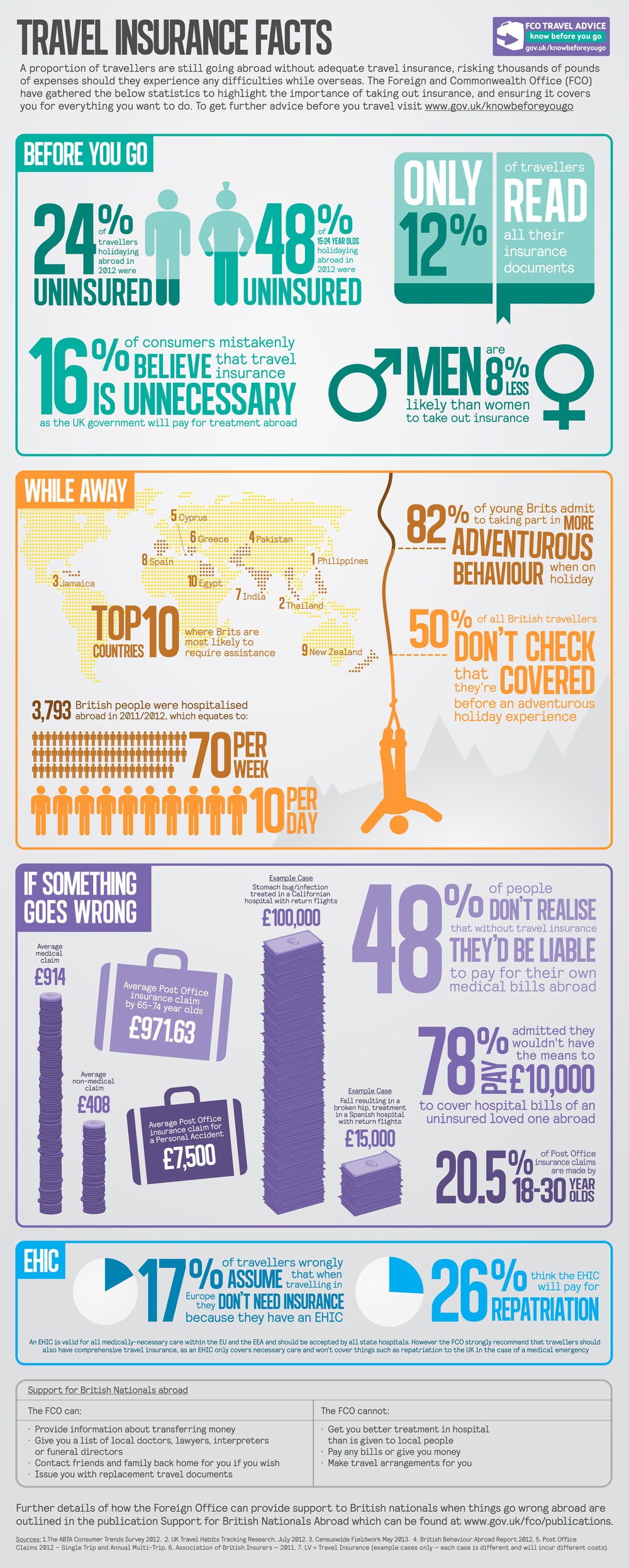

25% of holiday-goers in the run up to May 2017 didn’t have insurance, according to ABTA. That’s 3% more than shown in the data from May 2016. However, this differed between age ranges but was commonly problematic among young people travelling abroad.

In May 2016, 31% of 18-24-year-olds travelled overseas without insurance. This figure increased by 9% in the following year. 25-34-year-olds were also guilty of this risky move, with 31% of jet-setters not insured in 2016 — growing to 38% in 2017.

The 35-44-year-olds bracket displayed a decrease in the number of people going overseas without insurance for 2016 and 2017. However, this drop was marginal, down to 25% from 26%. For people aged 45-54, 20% of travelers weren’t insured for their trip in 2016, a figure that grew by 3% in 2017. Those aged 55 and over remained the same over the two years, with just 14% not taking out insurance before their trip.

But why are so many risking going on holiday without the appropriate insurance? 36% said that they didn’t think that they needed it. Although refusing to buy insurance will have short-term financial benefits, the savings made don’t compare to the detrimental financial situation you could be in if something was to go wrong abroad. Despite this, 22% said that it was a risk they were willing to take.

A large number of people think they don’t need insurance if they are travelling in Europe and have a European Health Insurance Card (EHIC). However, this is not the case, as EHIC is only valid for medical necessities within the European Union and the European Economic Area (EEA) in state hospitals. It has been advised by the Foreign and Commonwealth Office that all people wishing to travel outside of their country should also have comprehensive travel insurance as this will likely cover repatriation in the case of a medical emergency.

It’s not known what will happen yet in regard to EHIC and the effects of Brexit. What we do know is that those who are officially living abroad — whether this is to work or study on the day the UK officially leaves the EU — their card will continue to prove eligibility for the same state-funded healthcare as the citizens of the country receive.

Travel insurance: key points you should know

Travel insurance covers for any problems that may arise before your holiday, or when you reach your destination. It’s important that you purchase your insurance as soon as you book your holiday, as it can cover potential cancellations and pre-trip illnesses — it’s a small financial decision that can save you a fortune in the long run.

Before committing to a purchase, look over the different policies offered by travel insurance, as the amount of coverage will differ between different companies. It is unlikely that they will cover high-risk activities. It’s important to consider what type of holiday you’re going on — if it’s active like skiing, you must inform your insurer to get the best cover.

Don’t neglect the small print. For example, if you’ve consumed alcohol and need medical attention some insurance companies will reject your claim — in extreme cases, they could seek out court rulings and will supply the court with medical records that say you had alcohol in your blood. It’s important to remember that in hot countries, your body will absorb alcohol more easily too.

If you are the victim of theft while on holiday, your claim will need a strong grounding of evidence.

It’s worth noting that if your travel company goes out of business. your cover will cease. However, when it comes to the airline going out of business, you may be covered but could be required to pay an extra premium.

Companies can only waiver the decision to cover events such as natural disasters or acts of terrorism in exceptional circumstances.

Most common holiday mishaps

74-80% of deaths on holiday are caused by natural matters such as heart attacks, according to research. However, the same source found that 18-24% occur due to accidents and 2% from infectious diseases. Two thirds of holidaymakers worry about getting sick when they’re away, but it’s inevitable when results show that one in 20 trips can include sickness or injury.

Common causes of the most frequent injuries (slips, trips, and falls) abroad include poorly-maintained floors and uneven footing. Take note of signs to ensure you’re not at risk of injury through slippery or uneven floors.

Driving difficulties are faced frequently, given we drive on the left in the UK. You might be trying to follow directions or the GPS on your phone — but you must stay alert and not get distracted to avoid any type of road traffic accident.

Don’t feel like you can’t take part in sporting events abroad, but be aware of the risks. If you have concerns, you must ask the organisers as high risk activities can invalidate any insurance policies if you’re not properly protected.

The average medical claim cost for such an injury comes to £914. However, for 65-74-year olds, this cost increases to £971.63. One example provided by the FCO stated that one stomach bug infection that was treated in a Californian hospital cost £100,000, including return flights back home.

48% of holidaymakers don’t realise that any medical bills abroad would be theirs to cover if they don’t have insurance. 78% said that they wouldn’t be able to pay just £10,000 to cover the costs that could present themselves.

It’s important to understand what insurance can cover you for when abroad, and equally, what it doesn’t cover. With Brexit just around the corner, and the fate of the EHIC unknown, will we see an increase in the number of people taking out insurance?

Sources:

https://betravelwise.com/10-interesting-maybe-random-travel-safety-statistics/

https://www.theguardian.com/money/2016/may/15/travel-insurance-holiday-europe

https://www.telegraph.co.uk/travel/advice/alcohol-consumption-invalidate-travel-insurance/

https://www.ons.gov.uk/peoplepopulationandcommunity/leisureandtourism/articles/traveltrends/2016

http://www.thisismoney.co.uk/money/bills/article-4596054/Could-slash-cost-summer-holiday.html

https://abta.com/about-us/press/two-in-five-millennials-travelling-abroad-uninsured

https://abta.com/assets/uploads/general/Holiday_Habits_Report_2017.pdf

http://www.bbc.co.uk/news/uk-politics-eu-referendum-41125931

{kind=link}